I asked five AI models to analyze my asset allocation. My current portfolio satisfies me and reflects my worldview, but it evolved organically over the past few years rather than through a deliberate plan.

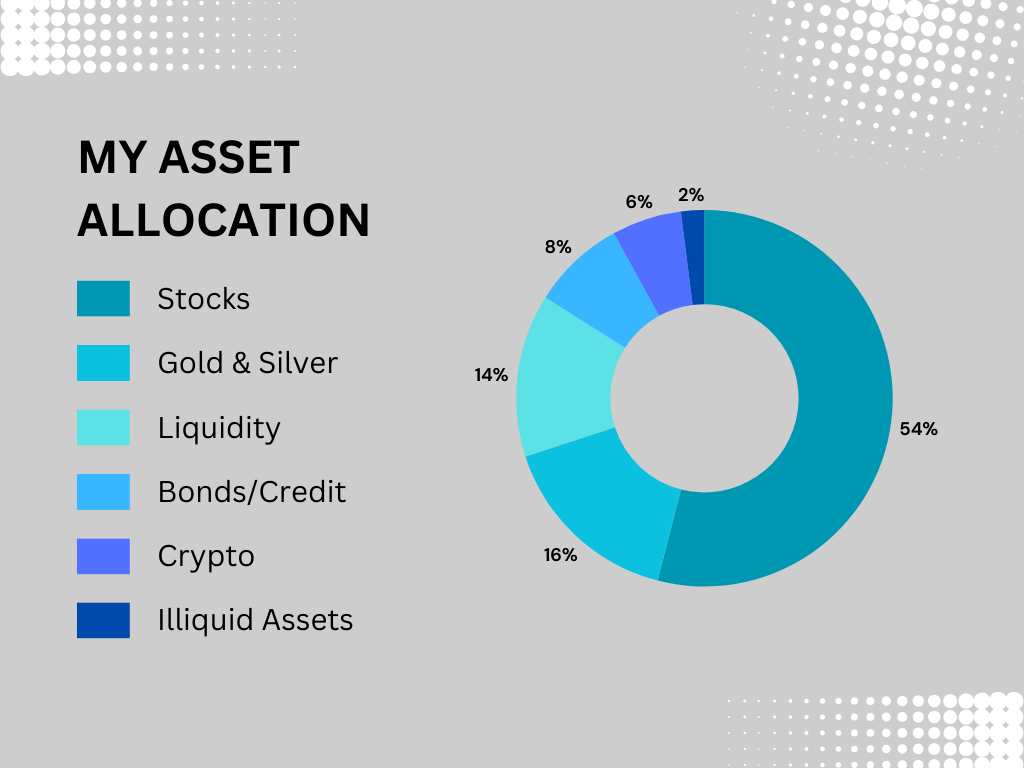

Portfolio A: stocks 54%, gold & silver 16%, liquidity 14%, bonds/credit 8%, crypto 6%, illiquid assets 2%

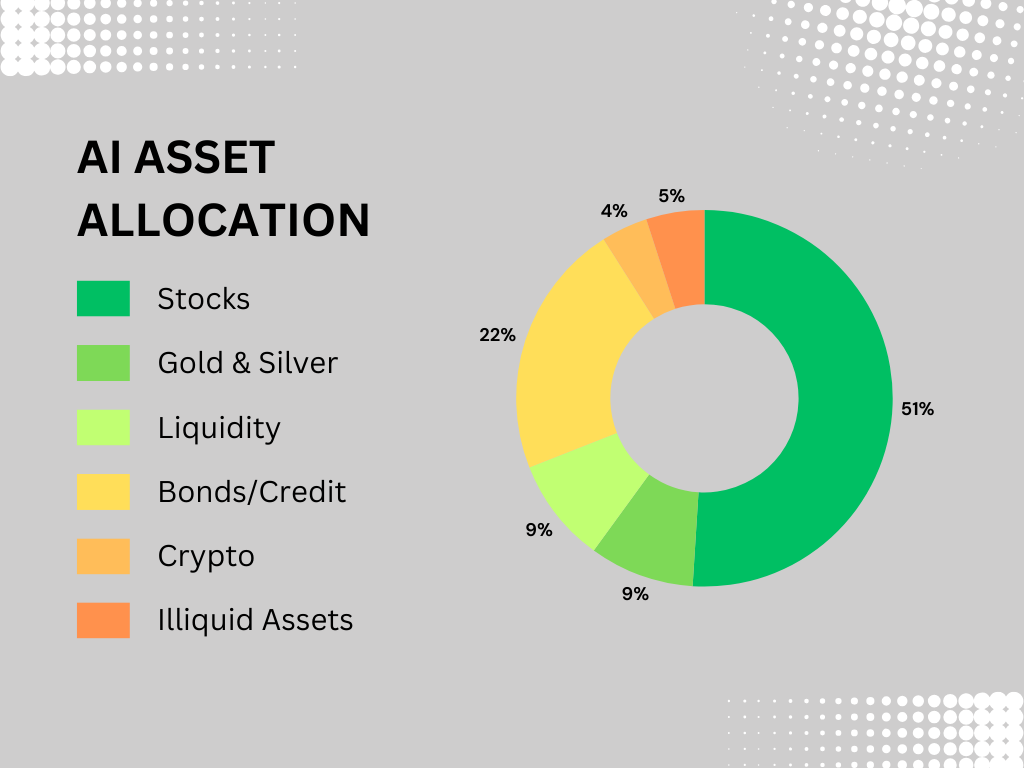

AI, however, leans heavily toward bonds, valuing their income, low volatility, and negative correlation with stocks during recessions. Their suggested allocation looks like this: stocks 51%, gold & silver 9%, liquidity 9%, bonds/credit 22%, crypto 4%, illiquid assets (real estate, cars…) 5% (Portfolio B)

Next, I asked them to assess the probability of three macro scenarios ten years from now and predict which portfolio would perform better in each.

Scenario 1 – Inflationary, fiscally dominated, hard‑asset world

- Structural inflation remains high (3–6%), not just a temporary spike.

- Governments run large deficits; central banks accommodate.

- Monetary debasement: liquidity injections, negative real rates, financial repression.

- High debt levels push policymakers toward inflation over austerity.

- Geopolitical fragmentation increases costs (US–China, Middle East, Europe).

- Commodity underinvestment constrains energy, metals, and infrastructure.

- Low productivity growth keeps real growth weak and inflation sticky.

Scenario 2 – Mild disinflation / soft landing

- Inflation gradually falls toward 2–3%, but not below.

- Central banks regain some credibility without crushing growth.

- Fiscal deficits remain high but manageable.

- Productivity improves modestly (AI, reshoring, capex cycles).

- Geopolitics remains tense but contained.

- Commodity prices stabilize rather than spike.

Scenario 3 – Deflationary recession

- Demand collapses due to recession, credit contraction, or financial crisis.

- Inflation drops sharply, possibly below 1%.

- Central banks cut rates aggressively; QE returns.

- USD strengthens as a safe haven.

- Fiscal stimulus is attempted, but deflation dominates temporarily.

- Productivity may rise paradoxically due to layoffs and capex cuts.

On average, AI sees Scenario 1 as most likely (45%), followed by Scenario 2 (37%) and Scenario 3 (18%). Portfolio A would outperform in Scenario 1, Portfolio B would slightly outperform in Scenario 2 and significantly in Scenario 3.

Finally, I asked the five bond‑biased AI which portfolio they would ultimately choose. Claude, ChatGPT, and Copilot pick A, while Gemini and Grok pick B.

Gemini also offered an unexpected insight: “Why on earth would I dump gold (a finite asset) for bonds (an infinite government promise)?”

Exactly – why on earth? 😉

There’s something genuinely interesting happening here – you’ve essentially used AI as a mirror and caught it contradicting itself. The models recommend Portfolio B, then when forced to choose under the scenarios they probability-weighted, three of five flip to Portfolio A.

That’s not a minor inconsistency. That’s the models’ training data (decades of 60/40 orthodoxy) fighting with their own scenario analysis in real time.

The Gemini line lands well, but be careful not to let a good quip do the heavy lifting. “Finite vs infinite promise” is rhetorically sharp, but gold’s actual performance case rests on real rates and dollar credibility – not just scarcity philosophy. Gold at $500 was finite too. The argument needs the macro scaffolding you’ve already built around it, not just the aphorism.

The 45% probability on Scenario 1 is also doing a lot of quiet work in your favor here. If you’d framed the same portfolio against a world where the models assigned 45% to Scenario 3, the conclusion flips entirely – and Portfolio A starts looking like an elegant way to lose purchasing power while feeling vindicated by your worldview. The scenarios aren’t neutral. They reflect your priors fed back to the models, which then confirmed them with probability weights. That’s a loop, not validation.

The organic evolution point is the most underexplored thread in the piece. A portfolio that “evolved organically” and happens to align with a coherent macro thesis is either genuine pattern recognition or survivorship narrative – and those feel identical from the inside.

You believe Scenario 1 is coming. Your portfolio bets on it. The AI agreed. At what point does that stop being analysis and start being a very sophisticated way of telling yourself what you already know?

If Scenario 2 quietly plays out for the next decade (the boring soft landing nobody wants to own intellectually), what does Portfolio A cost you, and would you actually change anything?

Leave a Reply