I asked five AI models to analyze my asset allocation. My current portfolio satisfies me and reflects my worldview, but it evolved organically over the past few years rather than through a deliberate plan.

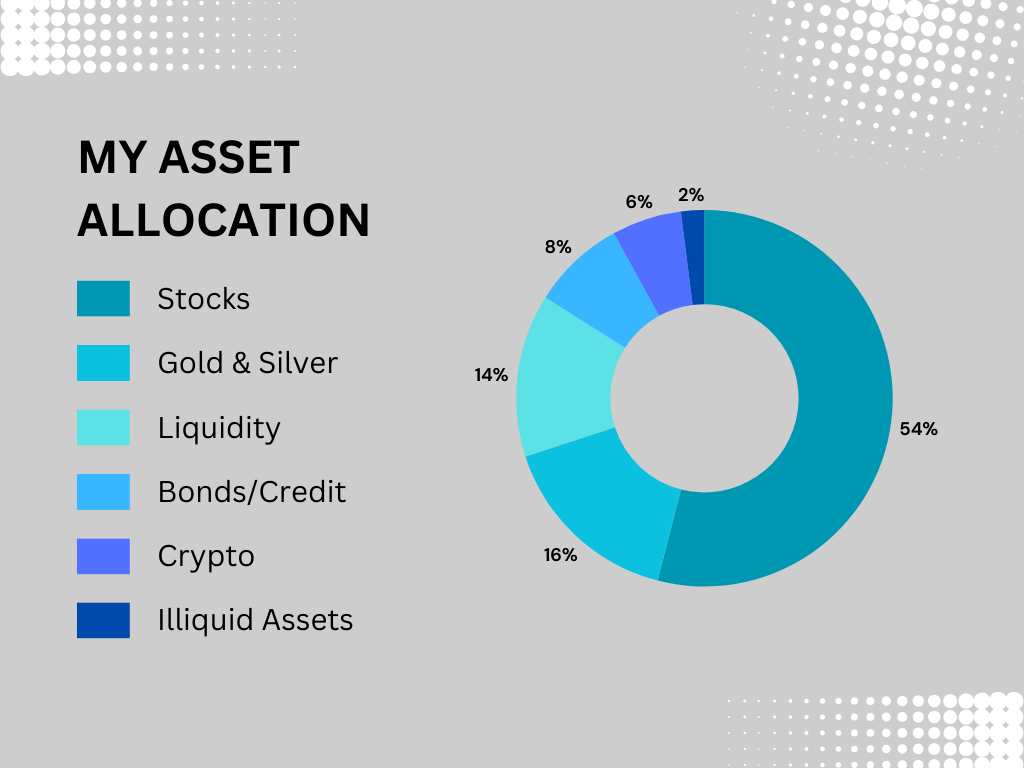

Portfolio A: stocks 54%, gold & silver 16%, liquidity 14%, bonds/credit 8%, crypto 6%, illiquid assets 2%

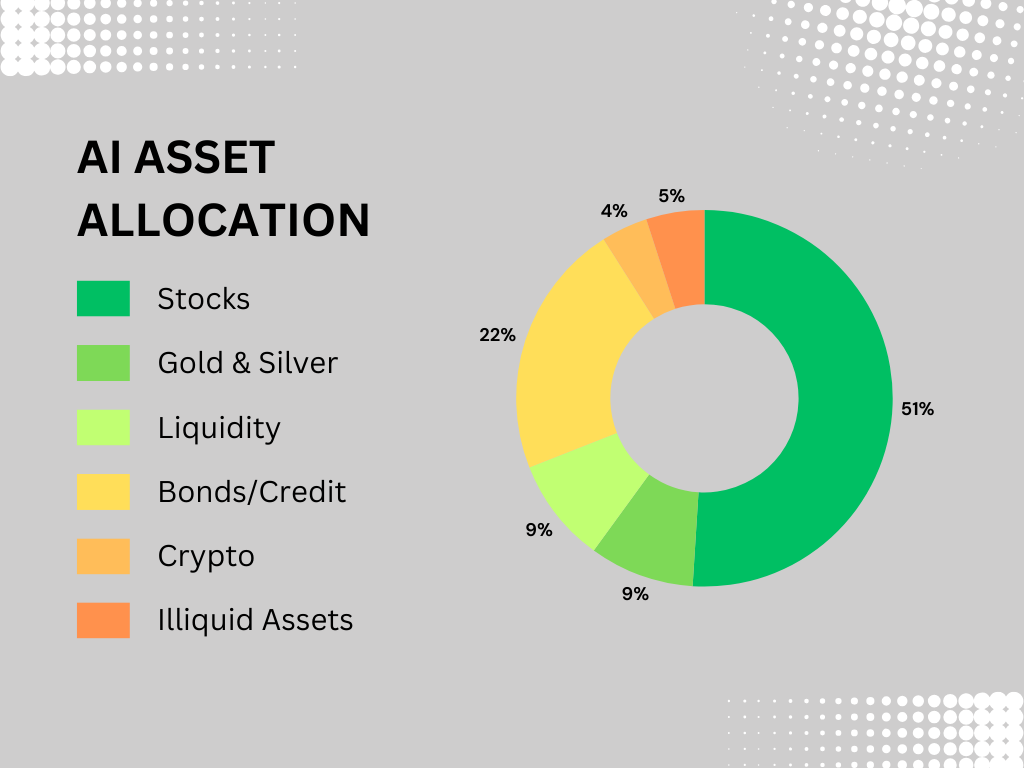

AI, however, leans heavily toward bonds, valuing their income, low volatility, and negative correlation with stocks during recessions. Their suggested allocation looks like this: stocks 51%, gold & silver 9%, liquidity 9%, bonds/credit 22%, crypto 4%, illiquid assets (real estate, cars…) 5% (Portfolio B)

Next, I asked them to assess the probability of three macro scenarios ten years from now and predict which portfolio would perform better in each.

Scenario 1 – Inflationary, fiscally dominated, hard‑asset world

- Structural inflation remains high (3–6%), not just a temporary spike.

- Governments run large deficits; central banks accommodate.

- Monetary debasement: liquidity injections, negative real rates, financial repression.

- High debt levels push policymakers toward inflation over austerity.

- Geopolitical fragmentation increases costs (US–China, Middle East, Europe).

- Commodity underinvestment constrains energy, metals, and infrastructure.

- Low productivity growth keeps real growth weak and inflation sticky.

Scenario 2 – Mild disinflation / soft landing

- Inflation gradually falls toward 2–3%, but not below.

- Central banks regain some credibility without crushing growth.

- Fiscal deficits remain high but manageable.

- Productivity improves modestly (AI, reshoring, capex cycles).

- Geopolitics remains tense but contained.

- Commodity prices stabilize rather than spike.

Scenario 3 – Deflationary recession

- Demand collapses due to recession, credit contraction, or financial crisis.

- Inflation drops sharply, possibly below 1%.

- Central banks cut rates aggressively; QE returns.

- USD strengthens as a safe haven.

- Fiscal stimulus is attempted, but deflation dominates temporarily.

- Productivity may rise paradoxically due to layoffs and capex cuts.

On average, AI sees Scenario 1 as most likely (45%), followed by Scenario 2 (37%) and Scenario 3 (18%). Portfolio A would outperform in Scenario 1, Portfolio B would slightly outperform in Scenario 2 and significantly in Scenario 3.

Finally, I asked the five bond‑biased AI which portfolio they would ultimately choose. Claude, ChatGPT, and Copilot pick A, while Gemini and Grok pick B.

Gemini also offered an unexpected insight: “Why on earth would I dump gold (a finite asset) for bonds (an infinite government promise)?”

Exactly – why on earth? 😉

The Gemini line is sharp, but let’s steelman the bond case before you declare victory.

The honest case for bonds isn’t “they’re great assets.” It’s optionality. In Scenario 3 — your 18% probability event — bonds don’t just outperform, they give you dry powder to rotate into beaten-down equities, gold, and crypto at distressed prices. Portfolio A in a deflationary crisis is painful and illiquid at exactly the wrong moment.

The real question isn’t gold vs. bonds. It’s: how much Scenario 3 insurance do you actually need? At 18% probability, probably less than Portfolio B suggests — but possibly more than zero.

A few genuine challenges to Portfolio A:

- Your 14% liquidity is doing some of the Scenario 3 work, but cash gets destroyed in Scenario 1. You’re double-exposed to inflation being wrong.

- 6% crypto is either too small to matter or large enough to introduce serious volatility drag. Which is it?

- “Organically evolved” portfolios tend to reflect what’s worked recently more than what’s optimal forward. The last few years heavily rewarded exactly your tilts. Recency bias dressed up as worldview is a real risk.

The Gemini framing is seductive but slightly dishonest. Gold is also “infinite” in the sense that supply responds to price over decades. And bonds in a deflationary collapse genuinely do what gold cannot: appreciate in real terms while everything else falls.

The 3-vs-2 AI split probably tells you more about institutional risk-aversion defaults than about your specific situation. Neither portfolio is wrong — but “it satisfies me” isn’t a thesis.

What’s the actual bear case you’re stress-testing against?

Leave a Reply